Current Market Conditions in the Global Passive Components Industry April 2015

05/19/2015 //

Introduction

This MarketEYE installment takes a closer look at the current market conditions in passive electronic components for 2015 and the historical trends with respect to currency valuations, lead time indicators, raw material pricing and vendor revenues.

Currency Headwinds

The major factor contributing to adverse market conditions in the global passive electronic component industry in April of 2015 is the continued weakening of foreign currencies to the U.S. dollar. This weakening of the yen, won and New Taiwan dollar is causing increased price competition in all regions of the world. The yen and won weakness to the U.S. dollar will continue to be the major factor impacting revenues of passive component vendors for the remainder of 2015.

The exchange rates of foreign currencies that define the passive component market index, have been having a major impact on vendors that report their revenues in U.S. dollars. Between October 1, 2014 and December 31, 2014 the yen value to the U.S. dollar increased by 10.2%, followed by an additional 4% gain in the March 2015 quarter. Both the won and the NT$ are also weakening to the dollar as is shown in Figure 1.0 below. The weakening of the won in the March 2015 quarter was greater than expected and this improved reporting for Korean vendors of passive components for the quarter when converted into U.S. dollars.

Summary Figure 1.0: Changes in Key Currency Valuations to The United States Dollar by Quarter: 2013-2015

Source: Compiled By Paumanok Publications, Inc. from public data. Currency exchange rates are the 90-day average price per quarter.

Paumanok Publications, Inc. estimates that the Yen, won and NT$ will continue to weaken in the June 2015 quarter which will create “headwinds” for Western passive component manufacturers and continue to generate a flat revenue rate on a quarter-to-quarter basis.

Lead Time Trends

The collective lead time index for passive electronic components had been in a volatile state on a month-to-month basis for the first half of 2014, but has been consistently improving since May of 2014, a trend which has continued into April of 2015. The lead-time index, which shows the average time in weeks that it takes for a passive electronic component manufacturer to deliver an ordered part to a customer, is extremely sensitive and responds to various impacts on the supply chain, both natural and man-made. For example, in the past the index has responded to the global economic stimulus packages of 2010 and 2011, and has also responded to the impact of the Tohoku earthquake in Japan and the flooding in Thailand in 2011. For all of 2012 and the balance of 2013 the lead-time index has expressed an anemic trend of relative inactivity. In the second half of 2014 and the first half of 2015 it is apparent that unit demand for capacitors, resistors and inductors has been steadily increasing to satisfy demand coming from Smartphone, tablet and automotive customers, however, the weakened yen, won and NT$ to the U.S. dollar is creating excessive price erosion in all world regions where vendors compete, thus creating almost no growth when measured in U.S. dollars (See Figure 2.0).

Figure 2.0: Global Lead Times (In Weeks) for Passive Electronic Components by Month: 2012-2015

Source: Paumanok Publications, Inc. Lead Times in Weeks

Raw Material Price Indicators

The raw material price index for passive electronic components is also an excellent indicator of economic conditions in the supply chain. Paumanok looks at key raw materials that are consumed by passive electronic component manufacturers and are considered major contributors to their overall cost of goods sold. Raw material price increases can have a major impact on the operating profit margins of component manufacturers, especially when currency valuations impact revenues. The types of materials that are tracked include base metal aluminum, nickel, copper, zinc; and precious and rare metal materials; palladium, ruthenium, silver, tantalite; as well as crude oil prices. What is interesting about these materials is that they are also used in many other end-use market segments as primary, secondary and additive materials and therefore their costs can have a major impact on vendor profitability. The passive component raw material index has been trending downward since 2011, which bodes well for helping to boost profit margins of passive component manufacturers; however, it also indicates the weakness of the greater global economy (See Figure 3.0). It is also important to note that changes in currency valuations are having less of an impact on raw material pricing because many feedstock materials are extracted in regions of the world that are not tied to the dollar, yen, won or NT$ and are (somewhat) insulated from fluctuations in various major currencies. However, feedstock pricing is more influenced by supply and demand status, and lower pricing reflects adequate inventory levels for key raw materials in the supply chain.

Figure 3.0: Average Selling Price per Ton for Feedstock Materials Consumed in The Passive Component Industry: 2009-2015

Source: Paumanok Publications, Inc. In US dollars

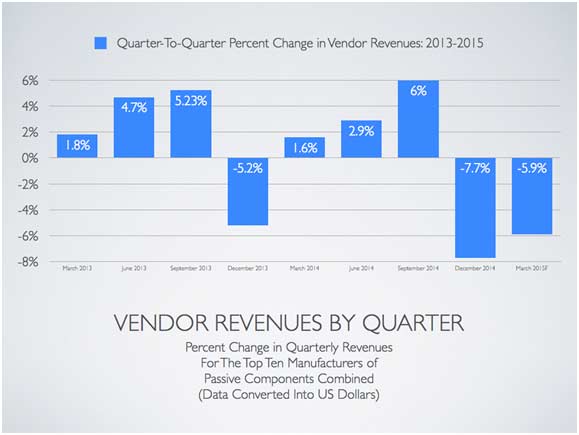

Change in Vendor Revenues

The percent change in quarter-to-quarter revenues for the world’s top 10 manufacturers of passive electronic components, which are measured in U.S. dollars and shown in the chart below (Figure 4.0), indicate the impact the weak yen, won and NT$ are having on collective revenue streams in passive electronic components. It is important to note that demand has shifted in favor of Japanese manufacturers of passive components because of the currency translation of the yen, whose continued weakness has had a positive impact on Japanese manufacturer’s revenues, as the inherent lower valuation gives Japanese vendors a global competitive advantage when responding to Requests For Quotes (RFQ) from OEM, EMS, and Distribution customers. Therefore, after single digit growth from March 2014 to September 2014 (when measured in U.S. dollars), the market slowed down in December 2014 and March 2015.

Figure 4.0: Quarter-To-Quarter Percent Change in Collective Passive Component Vendor Revenues: 2013-2015

Source: Paumanok Publications, Inc. Measured in U.S. Dollars Reflects Revenue change for respective divisions producing capacitors, resistors and inductors at the top ten manufacturers of passive components in the world for FY 2015.

Summary and Conclusions

The weak yen, won and NT$ to the U.S. dollar has been and will continue to be the most significant factor impacting global revenues in the passive component market for the remainder of 2015. The weak yen continues to create intense price competition regardless of geographic region and this is boding well for Japanese vendors of passive components at the expense of their American, Korean, Chinese and European counterparts. However, the increase in lead times suggests month-to-month increases in unit demand for capacitors, resistors and inductors to support growing demand from the Smartphone, tablet and automotive end-use market segments. Growth in units however is being offset by lower component pricing and this is creating a negative market environment for many vendors with respect to financial return on investment. Raw material pricing continues to come down, but as we noted, this is less an impact from currency valuations, and more from lack of materials demand from the larger global economy. The information in this MarketEYE piece is not all unfavorable. Unit demand continues to grow and raw material costs remain in check, however, it is apparent that the strength of the dollar is the deciding factor in providing adequate return on investment, and we do not see the yen, won or NT$ strengthening to the dollar in the near term, and this will create an anemic market environment for the balance of 2015, especially for those who measure their return in U.S. dollars.

Dennis M. Zogbi

Dennis M. Zogbi is the author of more than 260 market research reports on the worldwide electronic components industry. Specializing in capacitors, resistors, inductors and circuit protection component markets, technologies and opportunities; electronic materials including tantalum, ceramics, aluminum, plastics; palladium, ruthenium, nickel, copper, barium, titanium, activated carbon, and conductive polymers. Zogbi produces off-the-shelf market research reports through his wholly owned company, Paumanok Publications, Inc, as well as single client consulting, on-site presentations, due diligence for mergers and acquisitions, and he is the majority owner of Passive Component Industry Magazine LLC.